Introduction

Key Takeaways

- Credit score models like FICO and VantageScore calculate your creditworthiness differently, which can result in varying scores across platforms

- Lenders typically rely on specific credit score models when making lending decisions, and knowing which one they use can help you prepare

- Understanding the differences between major credit scoring systems empowers you to monitor the right metrics and improve your financial standing

- Your score can vary significantly depending on which model is used, even when based on the same underlying credit report data

- Different models weigh factors like payment history, credit utilization, and account age with varying importance

Hey there, it's Lexi. I learned about credit score models the hard way when I was car shopping and discovered my Credit Karma score didn't match what the dealership pulled. That eye-opening moment taught me that not all credit scores are created equal, and understanding which model lenders actually use is absolutely critical before any major financial move.

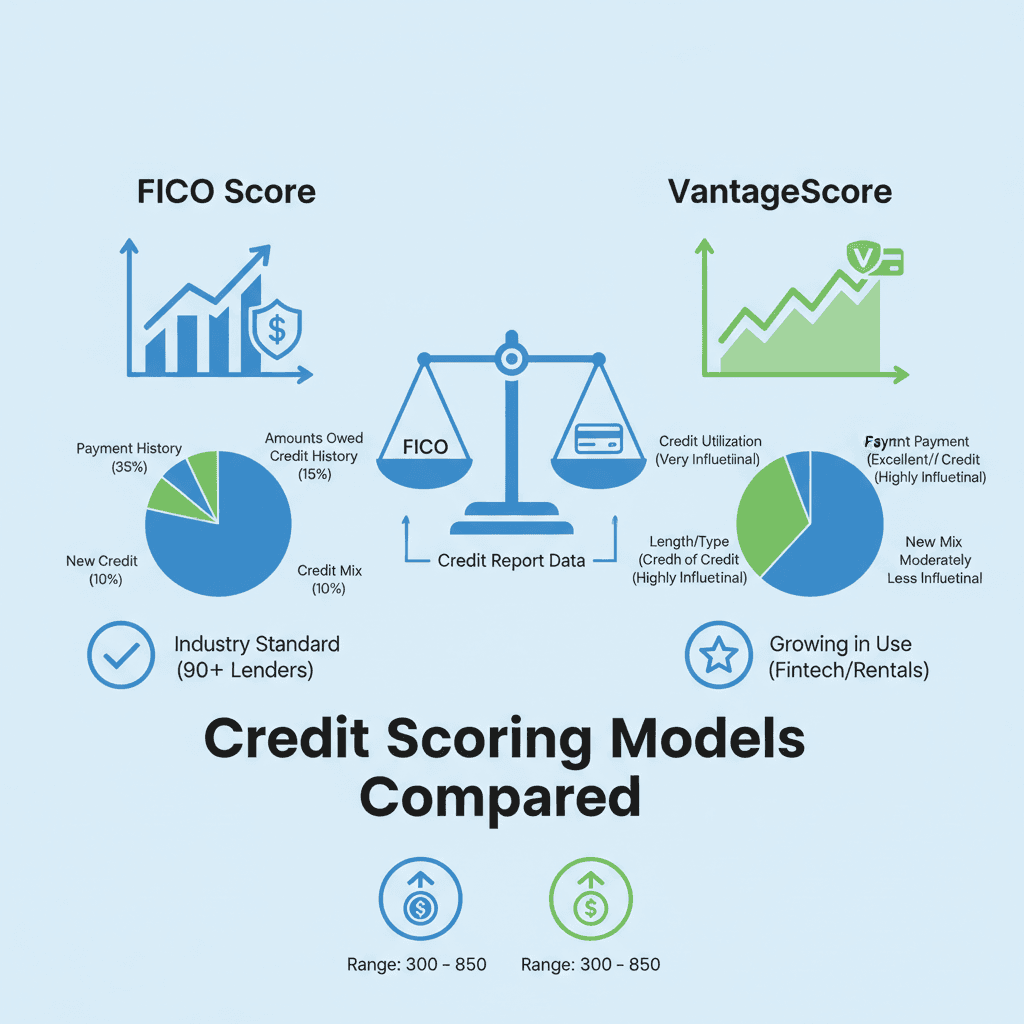

When you check your credit score, you might assume you're seeing the same number a lender will use to evaluate your loan application. The reality is far more complex. Multiple credit score models exist, each with its own formula for calculating your creditworthiness. The two dominant systems are FICO and VantageScore, and they can produce different scores from the same credit report.

This matters because lenders don't all use the same scoring model. Some rely exclusively on FICO scores, while others have adopted VantageScore or use proprietary models altogether. The score you monitor might not be the score that determines whether you get approved for a mortgage, auto loan, or credit card. Understanding these differences helps you prepare more effectively and avoid surprises during the application process.

The impact on your financial life can be significant. A score that looks healthy on one platform might appear lower when a lender pulls their preferred model. These variations aren't errors—they're the result of different methodologies, weighting systems, and data interpretation. Knowing which credit score models matter most for your specific financial goals puts you in control of your credit journey.

Explore the differences between FICO vs VantageScore and learn which credit score model matters more for lenders.

Focus keyword: credit score models

Tone: professional

Table of Contents

- Introduction — Introduce the importance of understanding credit score models and their impact on lending.

- Table of Contents

- Understanding Credit Score Models — Explain the significance of credit score models in finance and lending.

- What is FICO? — Detail the FICO score model, its history, and how it is used by lenders.

- What is VantageScore? — Detail the VantageScore model, its features, and its application in lending.

- FICO vs VantageScore: Key Differences — Direct comparison of the two credit score models highlighting key differences.

- Strengths and Weaknesses of Each Model — Analyze the strengths and weaknesses of FICO and VantageScore.

- Who Should Choose What? — Provide recommendations on which credit score model to use based on different financial situations.

- Common Questions About Credit Scores — Address frequently asked questions regarding FICO and VantageScore.

- Conclusion — Summarize the key points discussed and provide a final recommendation.

10 sections

Understanding Credit Score Models

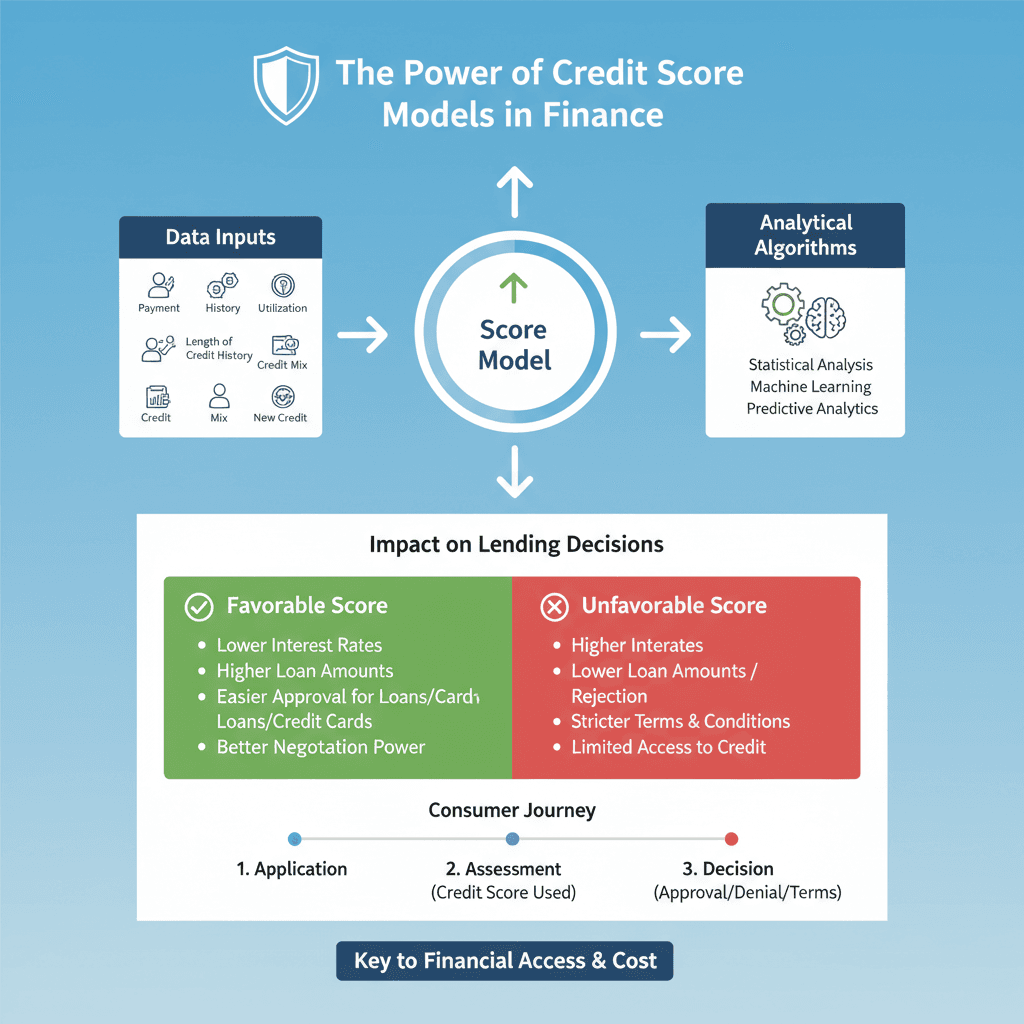

Credit score models are the mathematical formulas that lenders use to assess your creditworthiness. These models analyze your credit history and translate it into a three-digit number that helps financial institutions decide whether to approve your loan application, what interest rate to offer, and how much credit to extend. Understanding how these models work is essential for anyone looking to make informed financial decisions.

Different credit score models weigh factors differently, which is why you might see varying scores across platforms. The significance of these models extends beyond simple approval decisions—they directly impact the cost of borrowing money, from mortgages and auto loans to credit cards and personal loans.

The Core Components of Credit Score Models

While specific models may vary in their exact calculations, most credit score models evaluate similar categories of information. Payment history typically carries the most weight, accounting for approximately 35% of your score. This includes whether you've paid bills on time, any collections activity, and the recency of any missed payments.

Credit utilization—how much of your available credit you're using—contributes around 30% to your score. Experts generally recommend keeping your balances below 30% of your credit limit to maintain a healthy score. Length of credit history, new credit inquiries, and credit mix round out the remaining factors, with credit mix accounting for roughly 10% of your overall score.

Why Multiple Models Exist

The credit scoring landscape includes multiple models because different lenders have different priorities and risk tolerances. Some models are designed for specific types of lending, such as auto loans or mortgages, while others provide a more general assessment of creditworthiness. This variety allows lenders to choose the scoring model that best aligns with their particular lending criteria.

Recent changes in the industry have also influenced how models evolve. For instance, updates to medical debt reporting have removed most paid medical collections from credit reports, improving scores for many consumers. These ongoing adjustments reflect the industry's effort to create more accurate and fair assessments of consumer credit behavior.

The Impact on Your Financial Life

Your credit score model matters because it determines the financial opportunities available to you. A higher score typically translates to better interest rates, higher credit limits, and more favorable loan terms. Even a small difference in your interest rate can mean thousands of dollars in savings over the life of a mortgage or auto loan.

Understanding which model your lender uses helps you prepare more effectively for major financial decisions. While you can't control which model a lender chooses, focusing on the fundamental factors that all models consider—on-time payments, low credit utilization, and maintaining a diverse credit mix—will strengthen your profile across the board.

Sources

- Your 2026 Credit Score Playbook: What Really Moves …

- Your 2026 Credit Score Playbook: Changes, Tips & What …

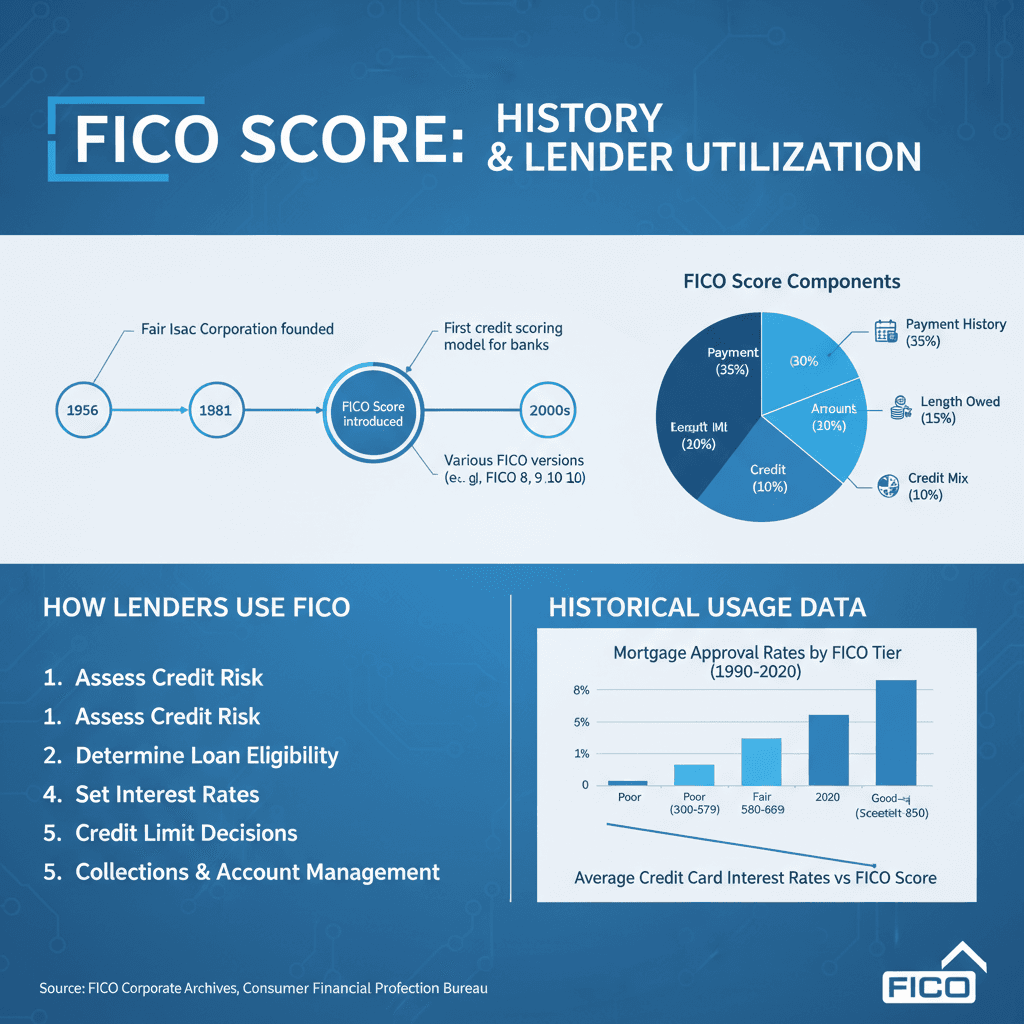

What is FICO?

FICO is the most widely used credit scoring model in the lending industry. Developed decades ago, it has become the standard tool that lenders rely on to assess creditworthiness when evaluating loan applications, credit cards, and mortgages. Understanding how FICO works is essential for anyone looking to improve their financial standing or prepare for a major borrowing decision.

How FICO Calculates Your Score

FICO scores are built on five key factors, each weighted differently. Payment history accounts for about 35% of your FICO score, making it the most influential component. This includes on-time payments, late payments, and any collections activity on your credit report.

Credit utilization contributes approximately 30% to your FICO score. Lenders recommend keeping your balances below 30% of your credit limit to maintain a healthy score. The length of your credit history, types of credit accounts, and recent credit inquiries make up the remaining percentages.

The Evolution of FICO Models

While the classic FICO scoring model has served lenders for years, newer versions have emerged to provide more nuanced assessments. Lenders are adopting FICO 10, which evaluates credit patterns over the past two years, emphasizing the importance of consistent credit habits rather than short-term fixes.

FICO 10T uses trended data to analyze 24 months of payment behavior. This version rewards consumers who actively reduce debt and penalizes those who only make minimum payments. The shift toward trended data means that your payment patterns from recent years now carry significant weight in determining your score.

Why Lenders Prefer FICO

FICO remains the dominant choice among lenders because of its proven track record in predicting credit risk. Banks, credit unions, and mortgage companies have built their underwriting systems around FICO scores, making it the gatekeeper for most lending decisions. Even as alternative models emerge, FICO's established reputation keeps it at the forefront of the industry.

Understanding which FICO version your lender uses can help you prepare more effectively. Some lenders still rely on older versions like FICO 8, while others have transitioned to newer models that incorporate trended data. Knowing the difference can give you a strategic advantage when applying for credit.

Sources

- Your 2026 Credit Score Playbook: What Really Moves …

- Credit Score Changes 2026 | Trended Data & New Models

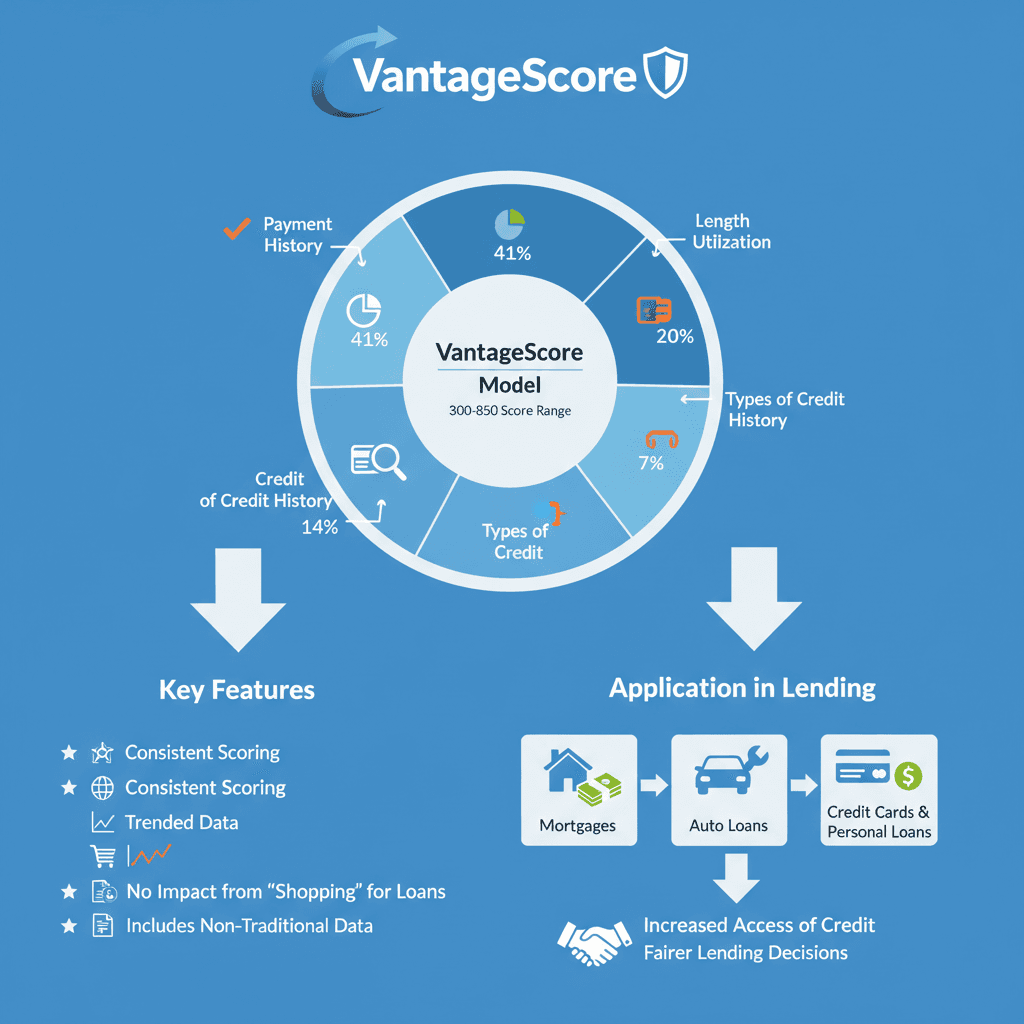

What is VantageScore?

VantageScore is a credit scoring model developed collaboratively by the three major credit bureaus. Unlike traditional models that rely solely on credit account history, VantageScore offers a more inclusive approach to evaluating creditworthiness. This model was designed to provide consistent scoring across all three bureaus and to expand credit access to consumers with limited credit histories.

Key Features of VantageScore

VantageScore uses a scoring range similar to other models, but its methodology differs in several important ways. The model can generate scores for consumers with as little as one month of credit history, making it particularly valuable for those new to credit. It also treats multiple inquiries within a short period as a single event, reducing the impact of rate shopping on your score.

One of the most significant developments is VantageScore 4.0, which mortgage lenders can now use. This newer version considers additional information such as rent, utilities, or telecom payments, helping those with limited credit histories establish creditworthiness. By incorporating these alternative data sources, the model provides a more comprehensive picture of financial responsibility.

Application in Lending

While VantageScore has gained traction in certain lending sectors, its adoption varies across the industry. Many credit monitoring services and financial apps display VantageScore because it provides consumers with a general sense of their credit health. The model's ability to score individuals with thin credit files makes it particularly useful for first-time borrowers or those rebuilding credit.

Rental history reporting has become increasingly important in credit scoring. By 2026, rental history reporting has become standard, with on-time rent payments weighted almost as heavily as mortgage payments. This shift benefits renters who consistently pay on time but may not have traditional credit accounts.

How VantageScore Differs in Practice

VantageScore tends to be more forgiving of recent credit recovery. If you've had past credit challenges but have been working to improve your financial habits, VantageScore may reflect your progress more quickly than other models. The scoring algorithm places emphasis on your most recent behavior, which can be advantageous for consumers actively rebuilding their credit profiles.

The model also handles medical collections differently than some traditional scoring systems, often giving less weight to medical debt that has been paid or settled. This approach recognizes that medical expenses can be unexpected and may not accurately reflect a person's overall financial management skills.

Sources

- Your 2026 Credit Score Guide: The Biggest Changes (and …

- Credit Score Mastery 2026: Navigating New Scoring Models

FICO vs VantageScore: Key Differences

While both credit score models evaluate your creditworthiness, they approach the task differently. Understanding these distinctions helps you interpret the scores you see and anticipate what lenders might review when you apply for credit.

Scoring Range and Scale

Both models use a range that typically spans from 300 to 850, making them superficially similar. However, the way they categorize risk within that range can differ. Each model has its own proprietary formula for translating your credit behaviors into a three-digit number.

Calculation Methodology

The core difference lies in how each model weighs credit factors. One model might place heavier emphasis on payment history consistency, while another might give more consideration to recent credit activity. These variations mean that the same credit report can yield different scores depending on which model is applied.

Recent updates have introduced trended data analysis in newer versions. Lenders are adopting models that evaluate credit patterns over the past two years, emphasizing the importance of consistent credit habits rather than short-term fixes. This shift means your behavior over an extended period now carries more weight than a single snapshot in time.

Treatment of Specific Credit Events

The models handle certain credit events differently. For instance, they may treat collections accounts, medical debt, or recent inquiries with varying levels of severity. One model might be more forgiving of a single late payment if your overall trend shows improvement, while another might penalize it more heavily.

Additionally, the minimum credit history required to generate a score can vary. Some models can produce a score with less credit history, making them potentially more accessible to individuals with thin credit files or those new to credit.

Industry Adoption and Usage

Lender preference plays a significant role in which score matters most to you. The financial industry has historically favored one model for certain types of lending, though adoption of alternative models has grown in recent years. Knowing which model your prospective lender uses gives you a clearer picture of where you stand in their evaluation process.

Sources

- Your 2026 Credit Score Guide: The Biggest Changes (and …

- Your 2026 Credit Score Playbook: Changes, Tips & What …

Strengths and Weaknesses of Each Model

Understanding the strengths and weaknesses of different credit score models helps you navigate the lending landscape more effectively. Each model has unique characteristics that can work for or against you depending on your credit behavior and financial situation.

FICO Model Strengths

FICO's primary strength lies in its widespread adoption across the lending industry. Most lenders rely on FICO scores when making credit decisions, which means this is often the score that truly matters for loan approvals and interest rates.

Newer FICO versions analyze payment behavior over time, rewarding consistent debt reduction. This approach benefits borrowers who demonstrate disciplined repayment patterns rather than simply making minimum payments.

FICO Model Weaknesses

FICO models can be less forgiving of recent credit missteps. Late payments and high utilization rates carry significant weight, which can make recovery from financial setbacks feel slower.

The model also requires a longer credit history to generate a score, which can disadvantage younger consumers or those new to credit. This creates a barrier for individuals trying to establish creditworthiness for the first time.

VantageScore Model Strengths

VantageScore can generate scores with less credit history, making it more accessible for people building credit from scratch. The model requires only one month of history and one account reported within the past two years.

This scoring system tends to give more weight to recent positive behavior, which can help consumers who are recovering from past financial difficulties. It offers a more dynamic view of creditworthiness that reflects current habits.

VantageScore Model Weaknesses

The main limitation of VantageScore is its limited use among lenders for actual credit decisions. While many free credit monitoring services display VantageScore, most lenders still pull FICO scores when evaluating applications.

This disconnect can create confusion when consumers see one score on monitoring apps but receive different scores during the lending process. The gap between what you monitor and what lenders see can lead to unexpected outcomes.

Optimizing Under Both Models

Regardless of which model a lender uses, certain practices improve scores across the board. Paying bills on time remains the single most important factor in any credit score model.

Keeping credit card balances manageable—ideally maintaining utilization under a certain threshold—benefits your score under both systems. Allowing accounts to age naturally also strengthens your credit profile over time.

Focusing on consistent principal payments rather than minimum payments demonstrates financial responsibility. This approach signals to both scoring models that you're actively managing and reducing debt, not just treading water.

Sources

- Your 2026 Credit Score Playbook: What Really Moves …

- Credit Score Changes 2026 | Trended Data & New Models

Who Should Choose What?

The truth is, you don't always get to choose which credit score model a lender uses. Most lenders have established preferences, and your job is to understand which model they rely on so you can manage your credit accordingly.

When FICO Matters Most

If you're applying for a mortgage, auto loan, or traditional credit card, lenders will almost always pull a FICO score. This model has been the industry standard for decades, and most financial institutions trust its methodology for assessing risk. Focus your efforts on understanding FICO's weighting of payment history and credit utilization if you're planning any major borrowing.

When VantageScore Comes Into Play

VantageScore appears more frequently in credit monitoring apps and educational tools. If you're using free credit tracking services to get a general sense of your credit health, you're likely seeing a VantageScore. While this can be helpful for spotting trends, remember it may differ from what lenders actually review.

The Smart Approach for Any Financial Situation

Regardless of which credit score models you encounter, the fundamentals remain consistent. Pay bills on time, keep credit utilization low, and avoid opening too many new accounts at once. These habits strengthen your credit profile across all scoring models.

Before applying for any loan or credit product, confirm which scoring model your lender uses. This simple step allows you to focus on the right credit habits and avoid surprises during the application process. Different models may weigh factors differently, but responsible credit management benefits you universally.

Sources

- Your 2026 Credit Score Playbook: Changes, Tips & What …

- Your 2026 Credit Score Guide: The Biggest Changes (and …

Common Questions About Credit Scores

Navigating the world of credit score models can raise many questions. Here are answers to some of the most frequently asked questions about FICO and VantageScore.

Which Credit Score Model Do Lenders Actually Use?

Lenders vary in their preferences, but FICO remains the dominant model in the lending industry. Most mortgage lenders, auto lenders, and credit card issuers rely on FICO scores when making credit decisions. However, some lenders have begun incorporating VantageScore into their evaluation processes, particularly for educational purposes or initial screenings.

Consumers should confirm which scoring model their lender uses. This allows you to focus on the credit habits that matter most for that specific model. Scores can vary between models, so knowing which one your lender checks helps set realistic expectations.

Why Do My Credit Scores Differ Across Platforms?

You may notice different scores when checking various credit monitoring services. This variation occurs because different platforms use different credit score models. For example, some free services display VantageScore, while lenders often pull FICO scores.

Additionally, scores can differ based on which credit bureau provides the data. Each bureau may have slightly different information on file, leading to score variations even within the same model.

How Do Recent Changes in Medical Debt Reporting Affect My Score?

Recent changes in medical debt reporting have removed most paid medical collections from credit reports. This policy shift has improved scores for many consumers who previously had medical debt impacting their creditworthiness.

Both FICO and VantageScore have adjusted their models to reduce the weight of medical collections. If you had paid medical debt on your report, you may have already seen a positive impact on your score.

What Factors Matter Most for Credit Score Models?

Regardless of which model is used, certain factors consistently carry the most weight. On-time payments remain the most critical factor in any credit scoring model. Payment history demonstrates your reliability as a borrower and has the greatest impact on your score.

Credit utilization and length of credit history also play significant roles. Keeping your credit card balances low relative to your limits and maintaining older accounts in good standing both contribute to stronger scores across models.

Can I Improve My Score Quickly?

While building excellent credit takes time, some actions can produce relatively quick improvements. Paying down high credit card balances reduces your utilization ratio, which can boost your score within a billing cycle or two.

Addressing errors on your credit report can also lead to immediate improvements. Review your reports from all three bureaus and dispute any inaccuracies you find. Correcting mistakes can result in score increases once the bureaus update your file.

Should I Monitor Both FICO and VantageScore?

Monitoring both models can provide a more complete picture of your credit health. While FICO scores are more commonly used by lenders, VantageScore offers valuable insights and may reflect positive changes more quickly in certain situations.

Many free credit monitoring services provide VantageScore access, making it easy to track trends over time. For major financial decisions like mortgage applications, consider obtaining your FICO scores directly to know exactly what lenders will see.

Sources

- Your 2026 Credit Score Playbook: What Really Moves …

- Your 2026 Credit Score Playbook: Changes, Tips & What …

Conclusion

Understanding credit score models is essential for anyone navigating the lending landscape. Throughout this guide, we've explored how FICO and VantageScore calculate your creditworthiness differently, examined their unique scoring ranges and methodologies, and identified which lenders prefer each model. The key takeaway is simple: FICO remains the dominant choice among most lenders, particularly for mortgages and auto loans, while VantageScore offers valuable insights for monitoring your credit health.

When preparing for major financial decisions, knowing which credit score model your lender uses can make all the difference. FICO tends to weigh payment history and credit utilization heavily, while VantageScore may be more forgiving of recent credit missteps if you're demonstrating recovery. Both models serve important purposes in the credit ecosystem.

From my own experience preparing to buy a car, I learned firsthand that the score you see on free monitoring apps might not match what lenders pull. I was confident with my VantageScore from Credit Karma, only to discover the dealership used FICO 8, which showed a different number. That moment taught me that not all credit score models are created equal, and understanding which one matters for your specific situation is crucial.

The best approach is to monitor both scores when possible, focus on the fundamentals that improve all credit score models—paying on time, keeping balances low, and maintaining a healthy credit mix—and always ask your lender which specific model they use before applying. By taking these steps, you'll be better prepared for any financial move and avoid surprises during the approval process.