Introduction

Key Takeaways

- Credit score models like FICO and VantageScore calculate your creditworthiness differently, leading to score variations across platforms

- Most lenders rely on FICO scores for lending decisions, making it the dominant model in the financial industry

- Understanding which credit score models lenders use can help you better prepare for major financial decisions like mortgages, auto loans, and credit cards

- Different scoring models weigh factors like payment history, credit utilization, and account age with varying importance

- Checking multiple credit score models gives you a more complete picture of your financial health

Hey there, it's Lexi. I learned the hard way that not all credit scores are created equal. When I was preparing to buy a new car, I felt confident about my Credit Karma score—only to discover at the dealership that lenders were using a completely different number. That eye-opening experience taught me the critical importance of understanding credit score models.

The reality is that your credit score isn't just one number. Multiple credit score models exist, and they calculate your creditworthiness using different formulas and criteria. The two most prominent models—FICO and VantageScore—can produce significantly different scores for the same person, which can feel confusing when you're trying to gauge your financial standing.

This matters because lenders don't all use the same scoring model. While you might see one score when checking your credit through a free app or credit monitoring service, the lender evaluating your loan application might be looking at an entirely different calculation. Understanding these differences empowers you to make informed decisions about your credit and helps you avoid surprises during critical financial moments.

In this guide, we'll break down how credit score models work, explore the key differences between FICO and VantageScore, and help you understand which model matters most for your specific financial goals. Whether you're applying for a mortgage, financing a vehicle, or simply working to improve your credit health, knowing how these models operate gives you a strategic advantage in managing your financial future.

Explore the differences between FICO vs VantageScore and learn which credit score model matters most for lenders.

Focus keyword: credit score models

Tone: professional

Table of Contents

- Introduction — Introduce the importance of understanding credit score models and their impact on lending.

- Table of Contents

- Understanding Credit Score Models — Explain what credit score models are and their relevance in the lending process.

- FICO Score Analysis — Analyze the strengths and weaknesses of the FICO score model.

- VantageScore Analysis — Analyze the strengths and weaknesses of the VantageScore model.

- FICO vs VantageScore Comparison — Provide a side-by-side comparison of key features and differences between FICO and VantageScore.

- Who Should Choose What — Guide readers on which credit score model to focus on based on their financial situation.

- Common Questions About Credit Scores — Address common questions regarding FICO and VantageScore to provide clarity.

- Conclusion — Summarize the key points and offer actionable advice on choosing the right credit score model.

9 sections

Understanding Credit Score Models

Credit score models are sophisticated algorithms designed to evaluate your financial reliability and predict the likelihood that you'll repay borrowed money. These models analyze your credit history and translate complex financial behaviors into a three-digit number that lenders use to make quick decisions about loan approvals, interest rates, and credit limits.

Think of credit score models as the language lenders speak when assessing risk. Just as different languages have unique grammar rules, different scoring models weigh financial factors differently. Some models might emphasize payment history more heavily, while others give greater consideration to credit utilization or the diversity of your credit accounts.

Why Multiple Models Exist

The lending industry relies on multiple credit score models because different types of loans require different risk assessments. A mortgage lender evaluating a 30-year commitment needs different insights than a credit card company offering revolving credit. Each model is calibrated to predict performance for specific lending scenarios, which is why you might see score variations across platforms.

The evolution of credit scoring reflects changes in consumer behavior and financial technology. Modern models are moving toward more comprehensive analyses that capture a wider range of financial behaviors, helping individuals with limited traditional credit histories demonstrate their creditworthiness through alternative data points.

The Role in Lending Decisions

When you apply for credit, lenders pull your score from one or more models to gauge risk quickly and consistently. Your score directly influences whether you're approved, what interest rate you receive, and how much credit you can access. A higher score signals lower risk, often translating to better terms and lower borrowing costs over time.

Understanding which model a lender uses matters because score variations can affect your financial outcomes. The scoring landscape is shifting toward behavioral analysis that reflects real-time financial patterns, including cash flow consistency and payment behaviors across various account types. This evolution means your credit score is becoming a more dynamic reflection of your current financial health rather than just a historical snapshot.

Sources

- Credit Score Mastery 2026: Navigating New Scoring Models

- Your 2026 Credit Score Playbook: Changes, Tips & What They Mean

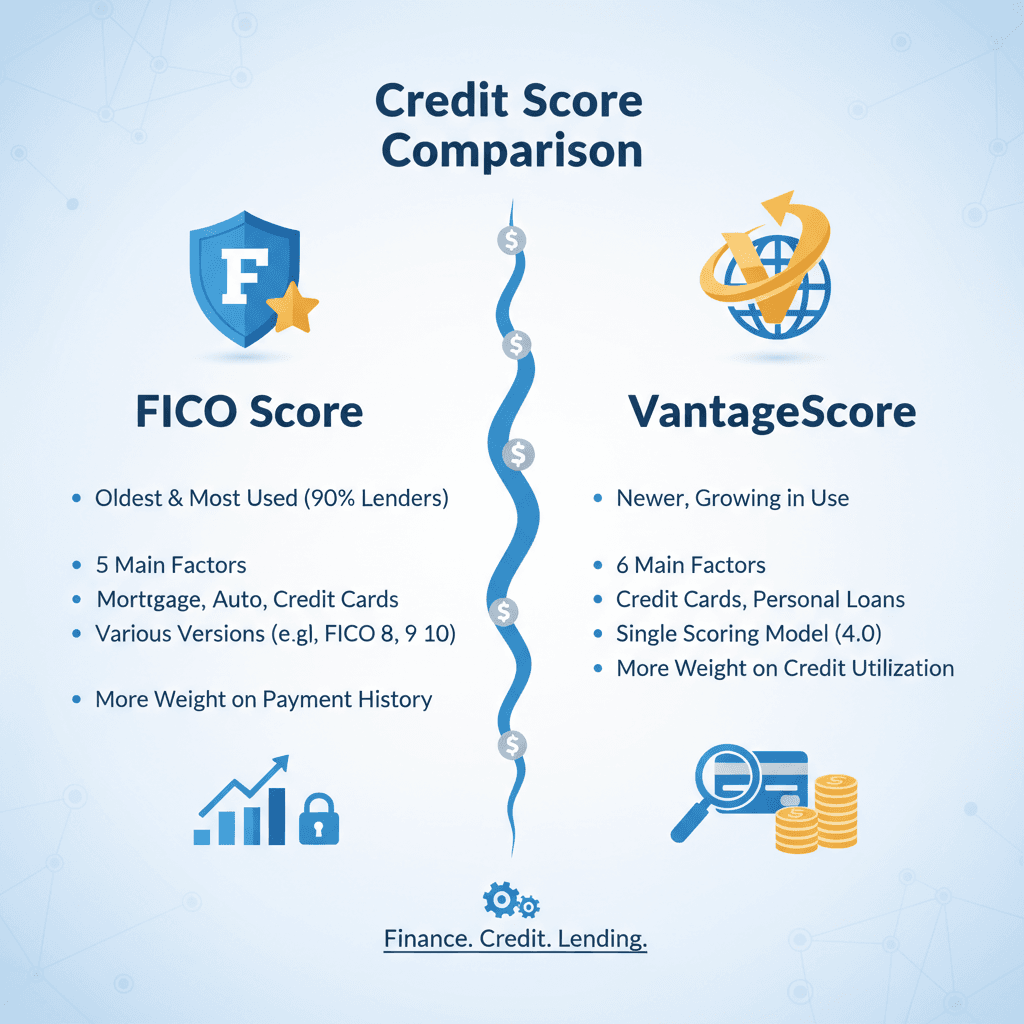

FICO Score Analysis

The FICO score model has been the dominant force in consumer lending for decades, and understanding its inner workings is essential for anyone looking to improve their creditworthiness. This model evaluates your credit behavior through a weighted system that prioritizes certain financial habits over others.

How FICO Weighs Your Credit Behavior

FICO's scoring methodology breaks down into five key components, each carrying different weight in your overall score. Payment history accounts for about 35% of your FICO score, making it the single most influential factor. This includes your track record of on-time payments and any collections activity that may appear on your report.

Credit utilization makes up about 30% of your FICO score. The model recommends keeping your balances below 30% of your available credit limit. For example, if you have a credit card with a $10,000 limit, maintaining a balance under $3,000 helps optimize this portion of your score.

The remaining factors include length of credit history (15%), new credit inquiries (10%), and credit mix, which contributes around 10% to your credit score. This last component rewards consumers who successfully manage various types of credit accounts, such as revolving credit cards alongside installment loans.

The Evolution to FICO 10

Lenders are increasingly adopting FICO 10, a newer version that evaluates credit patterns over the past two years rather than relying on a single snapshot. This shift emphasizes the importance of consistent credit habits and rewards borrowers who demonstrate sustained responsible behavior over time.

This evolution means that one-time improvements won't carry as much weight as maintaining good practices month after month. If you've been working to rebuild your credit, FICO 10 will recognize that sustained effort more favorably than previous versions.

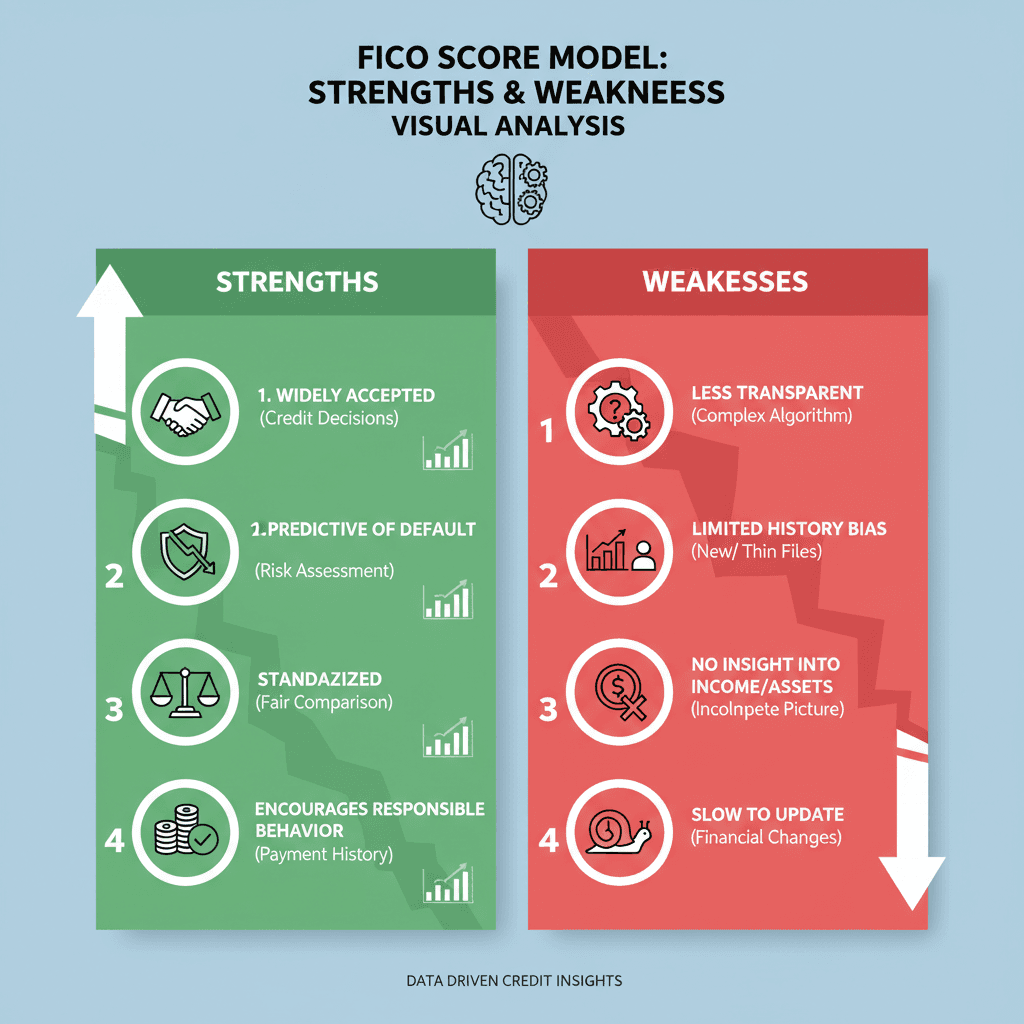

Strengths of the FICO Model

FICO's primary strength lies in its widespread acceptance across the lending industry. When you apply for a mortgage, auto loan, or credit card, there's a high probability the lender will pull your FICO score. This consistency makes it easier to understand what lenders see when evaluating your application.

The model's emphasis on payment history aligns well with what lenders care about most: whether you'll repay borrowed money on time. This straightforward approach has earned FICO its reputation as a reliable predictor of credit risk.

Weaknesses and Limitations

Despite its dominance, FICO has notable limitations. The model can be less forgiving for consumers recovering from financial setbacks. A single late payment can significantly impact your score, and the effects linger for years even after you've corrected your behavior.

FICO also requires a longer credit history to generate a score, which can disadvantage younger consumers or recent immigrants who haven't had time to build an extensive credit file. Additionally, the model doesn't always capture the full picture of financial responsibility, as it focuses primarily on credit accounts and doesn't consider factors like rent payments or utility bills unless they go to collections.

The weighted system, while transparent, can feel rigid. If you're rebuilding credit after a major life event, the heavy emphasis on payment history means recovery takes considerable time and patience.

Sources

- Your 2026 Credit Score Playbook: What Really Moves the Needle

- Your 2026 Credit Score Guide: The Biggest Changes (and What They …)

VantageScore Analysis

VantageScore emerged as a collaborative effort among the three major credit bureaus to create a more inclusive and consistent scoring model. While it hasn't achieved the same market dominance as FICO, VantageScore has carved out an important niche in the credit score models landscape, particularly for consumers with limited credit histories.

The model's evolution has been marked by continuous innovation. Each version has introduced features designed to address gaps in traditional credit scoring, making it easier for more Americans to access credit products.

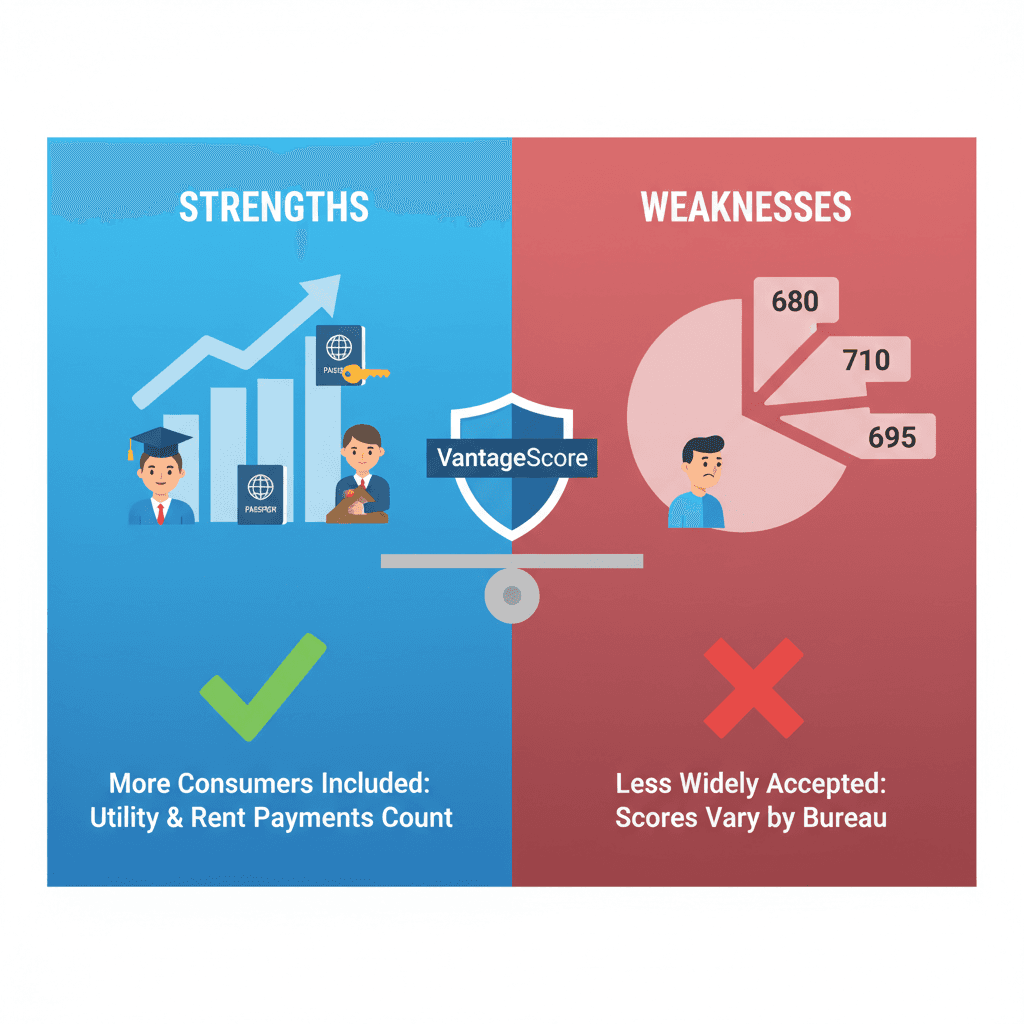

Strengths of the VantageScore Model

One of VantageScore's most significant advantages is its ability to score consumers with thin credit files. The model can generate a score with just one month of credit history and one account reported within the past 24 months. This approach opens doors for young adults, recent immigrants, and others who are just beginning their credit journeys.

VantageScore 4.0 represents a major advancement in scoring methodology. Mortgage lenders can now use this newer model, which considers additional information such as rent, utilities, or telecom payments, helping those with limited credit histories establish creditworthiness. This inclusive approach recognizes that responsible payment behavior extends beyond traditional credit accounts.

The model also treats trended data differently, analyzing patterns in your credit behavior over time rather than just providing a snapshot. If you're consistently paying down balances and demonstrating improving financial habits, VantageScore may reflect this positive trajectory more quickly than other models.

Weaknesses and Limitations

Despite its innovations, VantageScore faces a significant adoption challenge. Most lenders, particularly mortgage lenders and auto financiers, still rely primarily on FICO scores for lending decisions. This means your VantageScore might not be the number that matters when you apply for major credit products.

The scoring range consistency can be misleading. While VantageScore uses the same scale across all three bureaus, the actual scores can still vary significantly depending on the data each bureau has on file. This can create confusion when consumers see different VantageScore numbers from different sources.

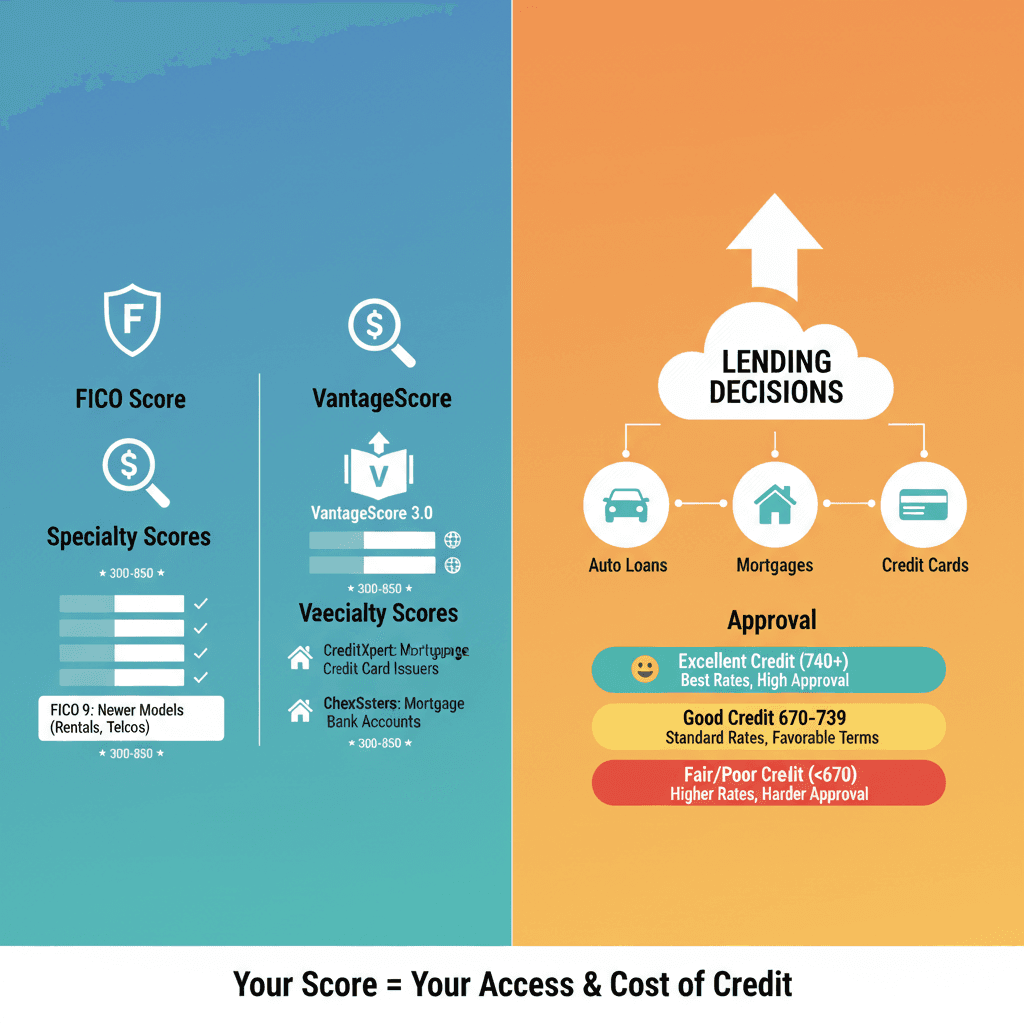

Another limitation is the relative lack of industry-specific models. While FICO offers specialized versions for auto loans, mortgages, and credit cards, VantageScore has fewer tailored variations. Lenders who want scoring models optimized for specific lending products may find FICO's specialized offerings more appealing.

Who Benefits Most from VantageScore

VantageScore serves certain consumer segments particularly well. If you're building credit from scratch, the model's ability to generate scores with limited history can help you monitor your progress and potentially qualify for starter credit products sooner.

Consumers who have experienced credit setbacks but are actively rebuilding may also benefit from VantageScore's approach. The model's treatment of medical collections and its focus on recent behavior can sometimes result in higher scores for individuals in recovery mode compared to traditional scoring models.

For everyday credit monitoring, VantageScore provides valuable insights into your credit health. Many free credit monitoring services use VantageScore, making it an accessible tool for tracking your financial progress even if it's not the score your lender ultimately checks.

Sources

- Your 2026 Credit Score Guide: The Biggest Changes (and What They …

- Your 2026 Credit Score Playbook: Changes, Tips & What They Mean …

FICO vs VantageScore Comparison

Understanding the differences between credit score models helps you navigate lending decisions with confidence. While both FICO and VantageScore aim to predict creditworthiness, they approach the task differently.

Score Range and Calculation Timing

Both models use a 300-850 score range, making them comparable at first glance. However, the timing of when they can generate scores differs significantly. FICO typically requires at least six months of credit history before producing a score, while VantageScore can generate scores with as little as one month of history. This makes VantageScore more accessible for consumers building credit from scratch.

How Payment History Is Weighted

Payment history remains the most critical factor in both models, but the weight varies. FICO traditionally emphasizes late payments heavily, treating them as strong negative signals. VantageScore takes a more nuanced approach, considering the context of your payment patterns and showing more flexibility for consumers recovering from financial setbacks.

Trended Data and Future-Looking Analysis

The landscape is evolving with newer versions of both models. Lenders are adopting FICO 10, which looks at credit patterns over the past two years rather than a single snapshot. This shift toward trended data means your credit behavior trajectory matters more than isolated incidents. The average mortgage FICO score increased from 715 to 760 due to the implementation of FICO 10T and VantageScore 4.0, reflecting how these newer models evaluate creditworthiness differently.

Credit Utilization Treatment

Both models penalize high credit utilization, but VantageScore tends to be slightly more forgiving of temporary spikes if your overall trend shows responsible management. FICO places consistent emphasis on keeping utilization below 30% across all reporting periods.

Industry Adoption Patterns

FICO dominates the lending industry, particularly for mortgages, auto loans, and credit cards. Most lenders use FICO scores for their underwriting decisions. VantageScore has gained traction in consumer credit monitoring services and some personal loan applications, but it remains the secondary choice for traditional lenders.

Which Score You'll See

When you check your credit through free monitoring services, you're often viewing your VantageScore. When a lender pulls your credit for a loan application, they're typically reviewing your FICO score. This discrepancy can create confusion, as the two scores may differ by 20-50 points or more depending on your credit profile.

Sources

- Your 2026 Credit Score Playbook: Changes, Tips & What They Mean

- Credit Score Changes 2026 | Trended Data & New Models

Who Should Choose What

The truth is, you don't really get to choose which credit score model lenders use—they make that decision for you. However, understanding which model matters most for your specific financial situation helps you monitor the right scores and focus your credit-building efforts where they'll have the greatest impact.

For most major lending decisions, lenders rely on specific scoring models tied to the type of credit you're seeking. Mortgage lenders typically use older versions of scoring models, while auto lenders and credit card issuers may use different versions altogether. This means the score you see on a free monitoring app might differ significantly from what your lender pulls.

Focus on What Lenders Actually Use

Before applying for credit, confirm which scoring model your lender uses. Call ahead or check their website to understand whether they pull a specific version and from which credit bureau. This simple step eliminates surprises and helps you understand any score differences you might encounter during the application process.

Once you know which model matters for your goal, you can monitor that specific score more closely. If you're planning to buy a home in the next year, for example, focus on the mortgage-specific scores rather than the general educational scores provided by free apps.

Strengthen the Fundamentals That Matter Everywhere

Regardless of which credit score model a lender uses, certain credit habits improve your standing across all scoring systems. Pay your bills on time every month without exception. Keep your credit card balances manageable—ideally below 30% of your available credit limits. Avoid opening unnecessary new accounts, especially in the months leading up to a major credit application.

These core practices move the needle on every credit score model because they demonstrate responsible credit management. While different models may weigh factors slightly differently, payment history and credit utilization remain critical components across the board.

Monitor Your Credit Reports Regularly

Regular credit report monitoring helps you catch errors, identify potential fraud, and track your progress over time. You're entitled to free credit reports from the major bureaus, and many financial institutions now offer free score monitoring as well.

By staying informed about what appears in your credit files, you can address issues before they impact your ability to secure favorable lending terms. This proactive approach matters more than obsessing over which specific score version a lender might use.

Sources

- Your 2026 Credit Score Playbook: Changes, Tips & What They Mean …

- Your 2026 Credit Score Guide: The Biggest Changes (and What They …

Common Questions About Credit Scores

Navigating credit score models can raise many questions, especially when you're trying to understand how lenders evaluate your creditworthiness. Here are answers to some of the most common questions about FICO and VantageScore.

How Do Recent Medical Debt Changes Affect My Score?

Recent changes in medical debt reporting have significantly improved credit scores for many consumers. Paid medical collections and debts under $500 have been removed from credit reports, which means if you previously had small medical bills affecting your score, they may no longer be holding you back. This policy shift recognizes that medical debt often doesn't reflect your overall financial responsibility in the same way other debts do.

Can Alternative Data Improve My Credit Score?

If you have a limited credit history or are rebuilding your credit, alternative data can be a game-changer. By opting into alternative data reporting—such as rent payments, utility bills, and subscription services—you can potentially gain significant points on your credit score. Some consumers have seen improvements of 50 to 100 points by including this additional payment history. This approach is particularly helpful for individuals who pay their bills on time but haven't established traditional credit accounts.

Why Do My Scores Differ Across Platforms?

You might notice different scores when checking various credit monitoring apps or when lenders pull your credit. This happens because different platforms use different credit score models. Some apps show your VantageScore, while lenders often use specific FICO versions. Additionally, the three credit bureaus (Equifax, Experian, and TransUnion) may have slightly different information about you, which can lead to score variations even within the same model.

Which Score Should I Monitor Regularly?

While monitoring any credit score helps you track trends and catch errors, it's most valuable to know which model your potential lenders use. For major financial decisions like mortgages or auto loans, focus on understanding the FICO versions those specific lenders prefer. For general credit health monitoring, any consistent score—whether FICO or VantageScore—can help you spot issues and track improvement over time.

How Often Do Credit Scores Update?

Your credit score updates whenever new information is reported to the credit bureaus, which typically happens monthly. However, not all creditors report on the same schedule, so you might see changes at different times throughout the month. Significant actions like paying down a large balance or opening a new account will eventually reflect in your score, but it may take 30 to 60 days for the full impact to appear.

Sources

- Your 2026 Credit Score Playbook: What Really Moves the Needle

- Credit Score Mastery 2026: Navigating New Scoring Models

Conclusion

Understanding credit score models is essential for making informed financial decisions. Throughout this guide, we've explored how FICO and VantageScore differ in their calculation methods, scoring ranges, and industry adoption. While both models aim to assess creditworthiness, FICO remains the dominant choice among lenders, particularly for mortgages and auto loans, while VantageScore offers a more accessible option for those with limited credit history.

The key takeaway is that not all credit score models are created equal. FICO's widespread use in lending decisions means it's often the score that matters most when you're applying for credit. However, VantageScore provides valuable insights into your credit health and can be particularly useful for monitoring your progress over time.

When preparing for major financial moves, check which credit score model your lender uses. This simple step can save you from surprises at the closing table. Request your FICO score directly from the credit bureaus or through your bank, and compare it with the VantageScore you might see on free credit monitoring apps.

Remember my experience at the dealership? I learned the hard way that knowing which model matters can make all the difference. Don't let different scores catch you off guard—arm yourself with knowledge about credit score models before making your next big financial decision. Whether you're buying a home, financing a car, or applying for a credit card, understanding these models puts you in control of your financial future.