Introduction

Key Takeaways

- Credit utilization measures how much of your available credit you're actively using and plays a significant role in determining your credit score

- The widely referenced 30 percent rule is often misunderstood, leading to confusion about optimal credit management strategies

- Understanding the nuances of credit utilization ratios can help you make informed decisions that positively impact your financial health

- Strategic timing and monitoring practices can enhance your credit profile beyond simply keeping balances low

Your credit score influences everything from loan approvals to interest rates, yet one of its most impactful components remains widely misunderstood. Credit utilization—the ratio of your current credit card balances to your total available credit—accounts for a substantial portion of your credit score calculation. Many consumers have heard the advice to keep utilization below 30%, but this guideline oversimplifies a more complex relationship between spending patterns and creditworthiness.

The reality is that credit utilization works differently than most people assume. While keeping your ratio low generally helps your score, the specific threshold, timing of payments, and reporting practices create opportunities for strategic management that go beyond the basic rule. Understanding these dynamics empowers you to optimize your credit profile without unnecessary restrictions on your spending.

This guide explores the mechanics of credit utilization, clarifies common misconceptions about the 30% threshold, and provides actionable strategies for managing your ratios effectively. Whether you're working to improve a damaged credit score or maintain an excellent rating, mastering utilization management is one of the most accessible tools in your financial toolkit.

Understanding Credit Utilization

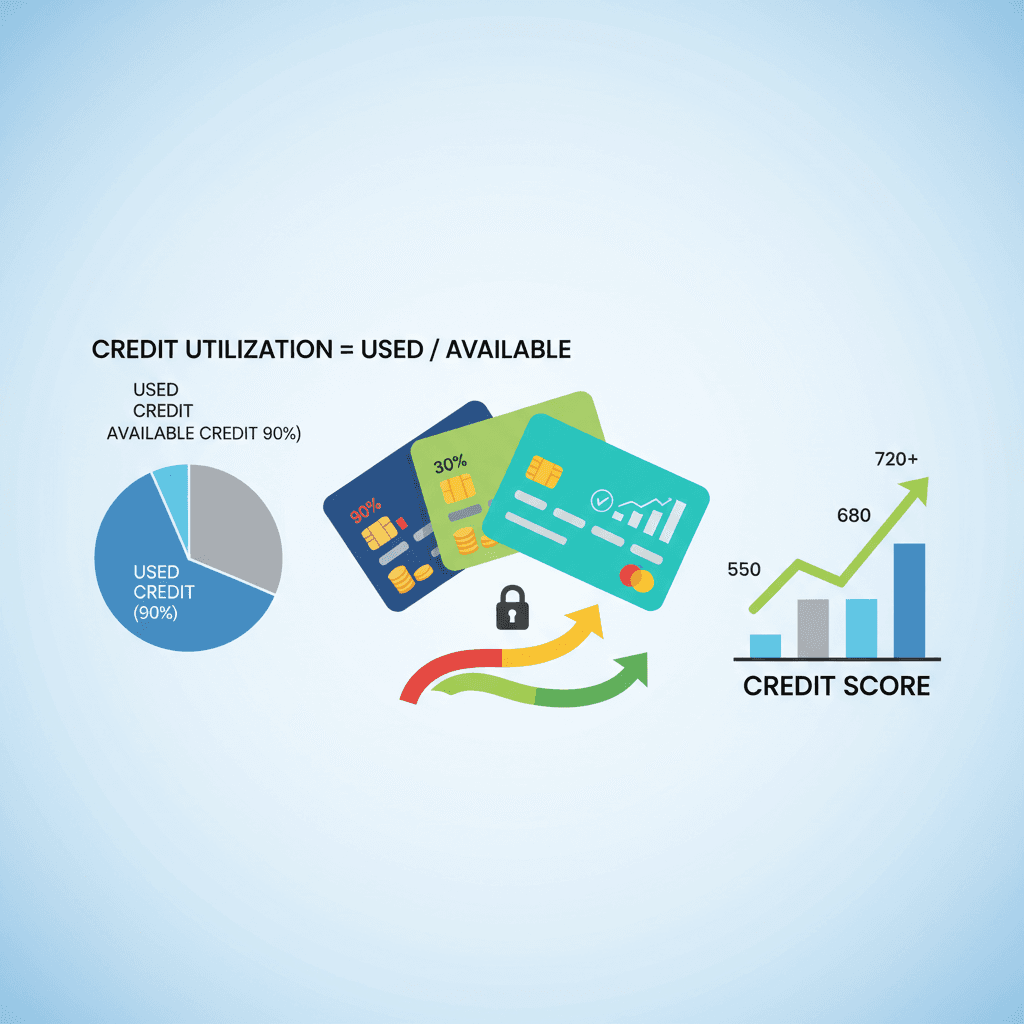

Credit utilization represents the percentage of your available credit that you're currently using. It's calculated by dividing your total credit card balances by your total credit limits across all accounts. For example, if you have $3,000 in balances across cards with a combined $10,000 limit, your utilization ratio is 30 percent.

This metric serves as one of the most influential factors in credit scoring models, typically accounting for approximately 30 percent of your FICO score calculation. Lenders view utilization as an indicator of financial health and borrowing risk. High utilization suggests you may be overextended financially, while lower ratios demonstrate responsible credit management.

How Utilization Is Calculated

Credit bureaus calculate utilization in two ways: per-card utilization and overall utilization. Per-card utilization examines each individual credit account separately, while overall utilization looks at your total debt-to-credit ratio across all revolving accounts. Both calculations matter, though overall utilization typically carries more weight in scoring algorithms.

Most credit scoring models update utilization figures based on the balance reported by your card issuer on your statement closing date. This means the balance on that specific date—not your payment due date—determines what appears on your credit report. Understanding this timing distinction becomes crucial for managing your credit profile strategically.

The Impact on Credit Scores

Lower utilization ratios generally correlate with higher credit scores. Research shows that individuals with the highest credit scores often maintain utilization below 10 percent, while those with lower scores frequently exceed 50 percent utilization. The relationship isn't linear, however—reducing utilization from 90 percent to 60 percent typically produces a smaller score improvement than reducing it from 30 percent to 10 percent.

Utilization changes can affect your credit score quickly because this factor has no memory in most scoring models. Unlike payment history, which remains on your report for years, utilization reflects only your current snapshot. This characteristic makes it one of the fastest ways to influence your credit score, either positively or negatively, depending on your spending patterns.

The 30% Rule Explained

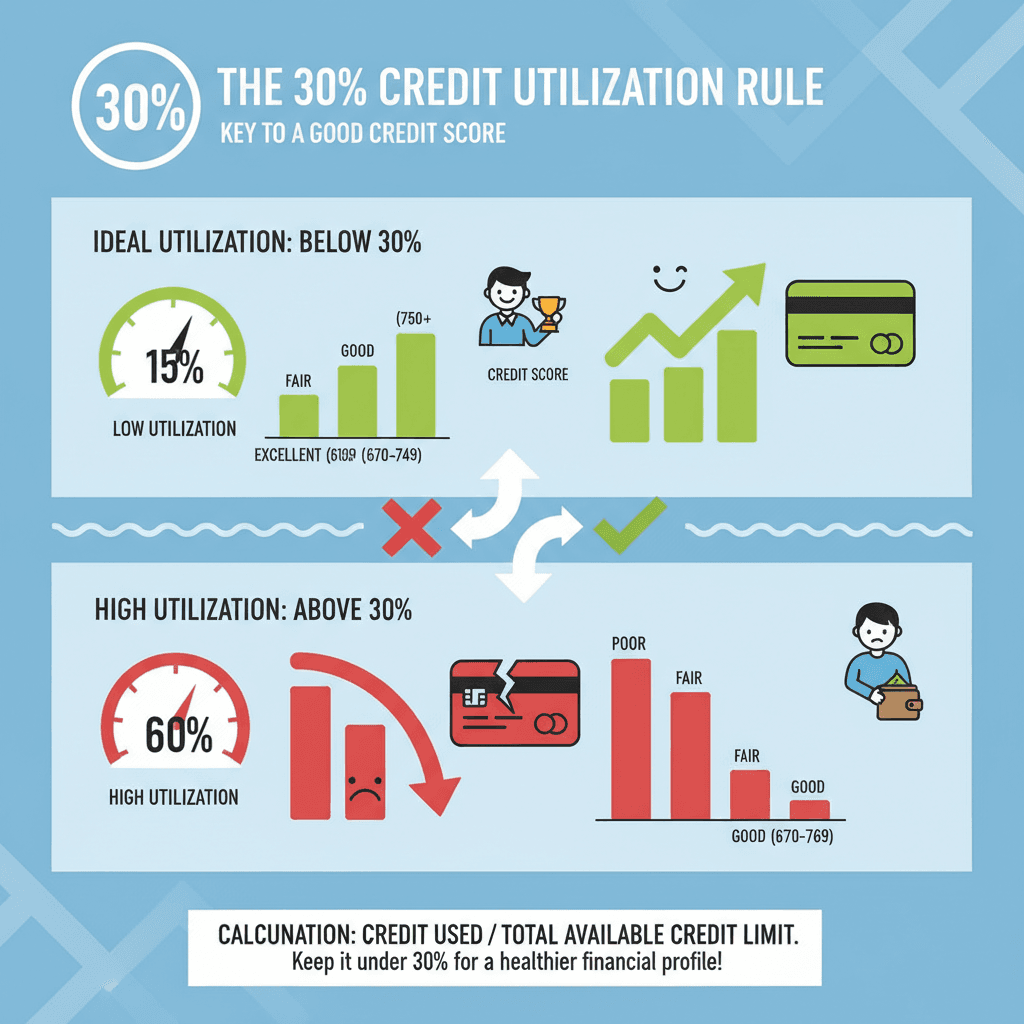

The 30 percent rule has become a widely recognized guideline in credit management, but its origins and true meaning are often misunderstood. This benchmark suggests keeping your credit utilization below 30% of your available credit limit. While the rule provides a helpful starting point, treating it as a rigid threshold can limit your credit score potential.

Many financial experts view the 30% marker as a floor rather than a ceiling. Staying below this percentage helps you avoid negative impacts on your credit score, but aiming even lower can yield better results. Credit scoring models reward lower utilization rates, with ratios under 10% often correlating with the highest credit scores.

Common Misconceptions About the Rule

One prevalent myth is that you must carry a balance to benefit from the 30% rule. In reality, you can use your credit cards regularly and pay them off in full each month while still maintaining optimal utilization. The key is understanding when your issuer reports your balance to credit bureaus.

Another misconception is that the rule applies uniformly across all credit types. While it's most relevant for revolving credit like credit cards, it doesn't directly affect installment loans such as mortgages or auto loans. These products follow different scoring considerations.

Why Lower Is Better

Think of the 30% rule as a minimum standard rather than a target. Credit scoring algorithms don't suddenly reward you for hitting 30% and penalize you at 31%. Instead, they operate on a sliding scale where lower utilization consistently produces better outcomes.

Consumers with excellent credit scores typically maintain utilization rates well below 30%, often in the single digits. This doesn't mean you can't use your available credit—it means strategic timing and payment practices can help you keep reported balances low while still leveraging credit for purchases and rewards.

Sources

- What is the 30% Rule in AI? Everything You Need to Know in 2026

- The 30% Rule for AI: A Practical Guide to Human-AI Collaboration in 2026

Myths About Credit Utilization

Credit utilization is often misunderstood, leading to confusion about how it truly affects your credit score. Many adults believe common misconceptions that can prevent them from optimizing their credit management strategies. By debunking these myths, you can make more informed decisions about managing your credit ratios effectively.

Myth 1: The 30 Percent Rule Is a Hard Limit

One of the most persistent myths is that keeping your credit utilization below 30% is a strict requirement for a good credit score. In reality, the 30 percent rule serves as a general guideline rather than a fixed threshold. While staying under 30% is beneficial, lower utilization rates—such as 10% or even single digits—typically correlate with even better credit scores. The rule should be viewed as a floor to avoid, not a ceiling to aim for.

Myth 2: Carrying a Small Balance Helps Your Score

Many people believe that carrying a small balance on their credit cards demonstrates responsible credit use and improves their score. This is false. Credit scoring models do not reward you for paying interest. What matters is your reported utilization ratio at the time your statement is generated. Paying your balance in full each month while maintaining low utilization is the most effective approach.

Myth 3: Closing Unused Cards Improves Utilization

Some assume that closing credit cards they no longer use will help their credit profile. However, closing accounts reduces your total available credit, which can actually increase your overall utilization ratio if you carry balances on other cards. Keeping unused cards open—provided they have no annual fees—helps maintain a lower utilization percentage across all your accounts.

Myth 4: Utilization Only Matters on Individual Cards

Another common misunderstanding is that credit utilization is calculated solely on a per-card basis. In fact, credit scoring models consider both individual card utilization and your overall utilization across all revolving accounts. Maxing out one card while keeping others at zero can still negatively impact your score, even if your total utilization appears reasonable.

Myth 5: Checking Your Credit Hurts Your Utilization Ratio

Some people worry that checking their own credit reports or scores will damage their credit or affect their utilization ratio. This is incorrect. Soft inquiries—such as checking your own credit—do not impact your credit score or utilization calculations. Regular monitoring is actually encouraged to ensure accuracy and track your progress.

Understanding these myths helps you navigate credit management with greater confidence. By recognizing what truly influences your credit utilization and score, you can adopt strategies that align with how credit scoring models actually work.

Sources

- The 30% Rule for AI: A Practical Guide to Human-AI Collaboration in 2026

- What is the 30% Rule for AI? - Vireo Sentinel

Improving Your Utilization Ratio

Managing your credit utilization ratio effectively requires a strategic approach that goes beyond simply paying down balances. By implementing targeted techniques, you can optimize your ratio and maintain a healthier credit profile over time.

Practical Strategies for Managing the 30 Percent Rule

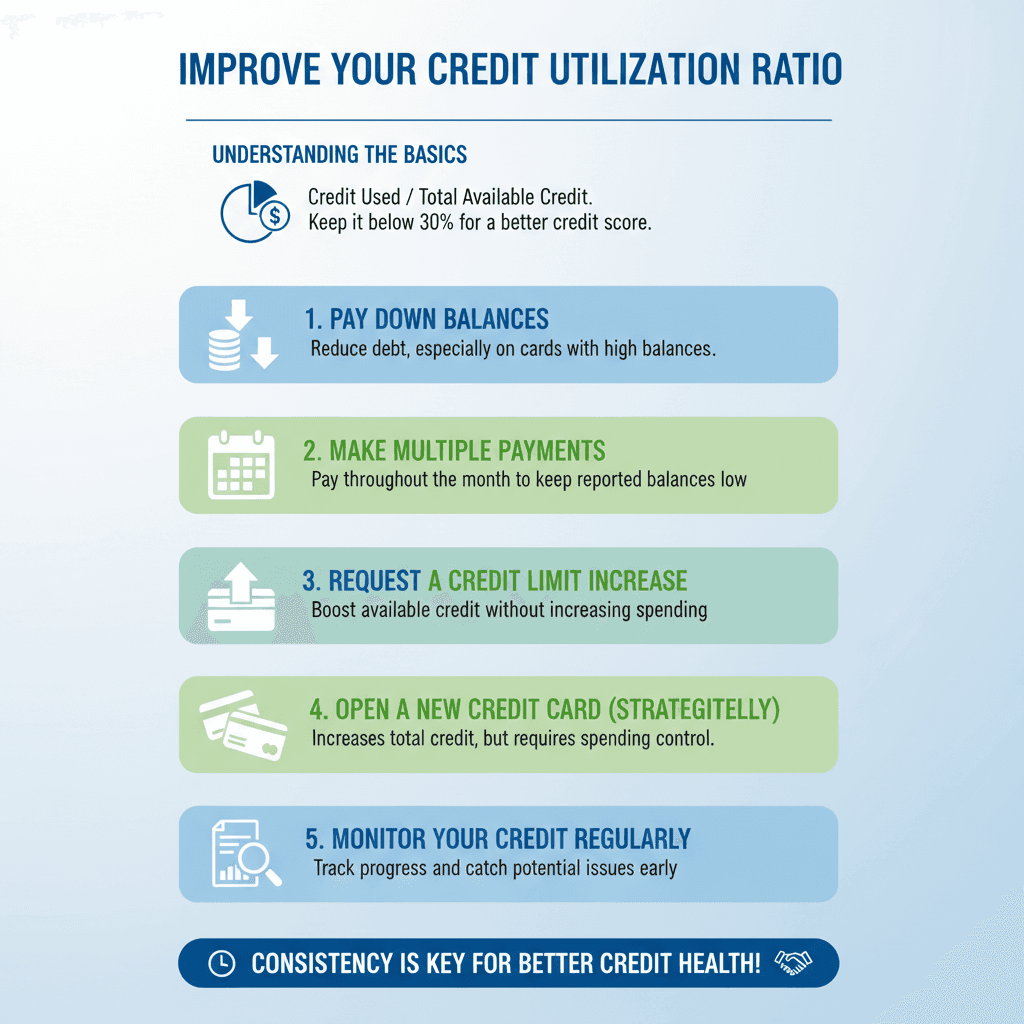

The most direct way to improve your utilization ratio is to reduce your outstanding balances. Focus on paying down cards with the highest utilization percentages first, as these have the most significant impact on your overall ratio. Even small reductions can make a measurable difference in how lenders view your creditworthiness.

Another effective strategy is to request credit limit increases on existing accounts. When your available credit rises while your balances remain the same, your utilization ratio automatically decreases. Contact your card issuers to inquire about limit increases, especially if you've demonstrated responsible payment behavior over several months.

Consider spreading charges across multiple cards rather than maxing out a single account. This approach helps keep individual card utilization low, which can be beneficial since lenders evaluate both your overall ratio and per-card ratios. Aim to keep each card well below the 30% threshold whenever possible.

Building Long-Term Ratio Management Habits

Develop a systematic approach to monitoring your credit usage throughout the month. Set up alerts through your card issuers to notify you when balances reach certain thresholds, allowing you to make strategic payments before utilization climbs too high.

Make multiple payments throughout your billing cycle rather than waiting for the due date. This practice keeps your reported balance lower and demonstrates active account management. You can schedule payments weekly or bi-weekly to align with your income schedule.

Avoid closing old credit card accounts unless absolutely necessary. When you close an account, you reduce your total available credit, which can increase your utilization ratio even if your spending habits haven't changed. Keeping accounts open—even if unused—helps maintain a favorable ratio.

Optimizing Your Credit Portfolio

If you're struggling with high utilization across multiple cards, consider consolidating debt through a balance transfer card or personal loan. This approach can lower your credit card utilization immediately, though it's important to avoid accumulating new balances on the cleared cards.

For those with limited credit history, becoming an authorized user on someone else's well-managed account can provide an immediate boost to your available credit. The primary cardholder's positive payment history and low utilization can benefit your credit profile as well.

Regularly review your credit reports to ensure all limits are accurately reported. Sometimes creditors fail to update increased limits with the credit bureaus, which can make your utilization appear higher than it actually is. Dispute any inaccuracies promptly to reflect your true credit situation.

Sources

- The 30% Rule for AI: A Practical Guide to Human-AI Collaboration in 2026

- What is the 30% Rule for AI? - Vireo Sentinel

The Statement-Date Timing Trick

One often-overlooked strategy for managing your credit utilization involves understanding when your credit card issuer reports your balance to the credit bureaus. Most issuers report your balance on your statement closing date, not your payment due date. This timing distinction creates an opportunity to influence the utilization ratio that appears on your credit report.

How Statement-Date Timing Works

Your statement closing date is typically several weeks before your payment is due. If you wait until the due date to pay your balance, the higher balance from your statement date has already been reported to the bureaus. By making a payment before your statement closes, you can reduce the reported balance and lower your utilization ratio.

For example, if you have a $5,000 credit limit and spend $2,000 during your billing cycle, your utilization would be 40% if reported at statement close. However, if you make a $1,000 payment before the statement closes, only $1,000 gets reported, resulting in a 20% utilization ratio.

Implementing the Strategy

To use this approach effectively, identify your statement closing dates for each credit card account. Most issuers list this date on your monthly statement or in your online account portal. Set a reminder a few days before each closing date to review your current balance.

If your balance is higher than your target utilization threshold, make a payment before the statement closes. You can make multiple payments throughout the month rather than waiting for a single payment at the due date. This proactive approach ensures the credit bureaus receive a lower utilization figure.

Potential Impact on Credit Scores

The statement-date timing strategy can have a meaningful impact on your credit scores, particularly if your reported utilization has been consistently high. Since utilization accounts for a significant portion of your credit score calculation, even small reductions in your reported ratio can translate to score improvements.

This technique is especially valuable when you're preparing for a major credit application, such as a mortgage or auto loan. By strategically timing your payments in the months leading up to your application, you can present the strongest possible credit profile to lenders.

Keep in mind that this strategy requires consistent attention and planning. Missing a statement date means waiting another month for the lower utilization to be reported. Additionally, always ensure you still make at least the minimum payment by your due date to avoid late fees and negative marks on your credit report.

Monitoring Your Credit

Regular monitoring of your credit score and utilization ratios is essential for maintaining healthy credit and catching issues before they impact your financial goals. By keeping a close eye on these metrics, you can identify trends, spot errors, and make informed decisions about your credit management strategy.

Why Regular Monitoring Matters

Checking your credit regularly allows you to track how your utilization ratio affects your credit score over time. Small changes in your balances can have measurable impacts, and monitoring helps you understand which actions produce the best results. Additionally, regular reviews help you catch unauthorized charges, reporting errors, or signs of identity theft early, giving you time to address problems before they escalate.

Consistent monitoring also keeps you accountable to your credit goals. When you see your progress reflected in improved scores or lower utilization percentages, it reinforces positive financial habits and motivates continued responsible credit use.

Tools for Tracking Credit Utilization

Many financial institutions now offer free credit score tracking through online banking platforms and mobile apps. These tools typically update monthly and provide basic insights into factors affecting your score, including utilization ratios. Some services break down utilization by individual account, making it easier to identify which cards need attention.

Credit monitoring services can provide more comprehensive tracking, including alerts when your utilization crosses certain thresholds or when new accounts appear on your report. While some premium services charge fees, many free options deliver sufficient functionality for most consumers' needs.

Establishing a Monitoring Routine

Set a regular schedule for checking your credit information—monthly reviews work well for most people. Mark a specific date on your calendar, such as the first of each month, to review your credit score, utilization ratios, and account activity. This routine helps you stay proactive rather than reactive with your credit management.

During each review, compare your current utilization to previous months and note any significant changes. Document your observations to identify patterns and measure progress toward your credit goals. This historical perspective provides valuable context that a single snapshot cannot capture.

Acting on What You Discover

Monitoring only provides value when you act on the information you gather. If you notice your utilization creeping above the 30 percent rule threshold, implement strategies to reduce balances before your next statement date. When you spot errors on your credit report, dispute them promptly with the relevant credit bureau.

Use monitoring insights to refine your credit strategy continuously. If certain payment timing approaches work better for your situation, adjust your routine accordingly. The goal is to create a feedback loop where monitoring informs action, and action improves the metrics you monitor.

Conclusion

Managing your credit utilization effectively is one of the most powerful tools available for building and maintaining a strong credit score. Throughout this guide, we've explored the fundamental principles behind credit utilization ratios, demystified the widely-referenced 30 percent rule, and uncovered strategic approaches that go beyond conventional wisdom.

Understanding that credit utilization accounts for a significant portion of your credit score calculation empowers you to make informed decisions about how you use your available credit. Whether you're maintaining low balances, timing payments strategically around statement dates, or requesting credit limit increases to improve your ratio, each action contributes to your overall financial health.

The myths we've addressed—from the misconception that carrying a balance improves your score to misunderstandings about how multiple cards affect your utilization—highlight the importance of working with accurate information. Knowledge replaces guesswork, allowing you to optimize your credit management with confidence.

Proactive management is key. Regularly monitoring your credit utilization ratio, staying aware of your statement closing dates, and making strategic payments throughout the month can create measurable improvements in your credit profile. These aren't one-time fixes but ongoing habits that support long-term financial success.

As you move forward, remember that credit utilization is dynamic—it changes with every purchase and payment. By implementing the strategies discussed here and maintaining consistent monitoring practices, you position yourself to achieve and sustain the credit score you need for major financial milestones. Take control of your credit utilization today, and watch your financial opportunities expand.

Discover credit utilization tips, including the 30% rule and statement-date strategies, to boost your credit score effectively.

Focus keyword: 30 percent rule

Tone: professional

Table of Contents

- Introduction — Introduce the concept of credit utilization, explain its significance in credit scoring, and set the stage for myth-busting the 30% rule.

- Understanding Credit Utilization — Define credit utilization, explaining what it is and how it affects credit scores.

- The 30% Rule Explained — Discuss the origins of the 30% rule, common misconceptions, and why it should be viewed as a floor rather than a ceiling.

- Myths About Credit Utilization — Debunk common myths surrounding credit utilization, highlighting why many adults misunderstand its implications.

- Improving Your Utilization Ratio — Provide practical strategies for managing and improving credit utilization ratios effectively.

- The Statement-Date Timing Trick — Explain the statement-date strategy, how it works, and its potential impact on credit scores.

- Monitoring Your Credit — Discuss the importance of regularly monitoring credit scores and utilization ratios, along with recommended tools.

- Conclusion — Summarize key points discussed, reiterate the importance of understanding credit utilization, and encourage proactive management.

- Table of Contents

9 sections